DAILY ANALYSIS 28 september 2022

- US indices finished yesterday’s trading mixed after a volatile session. S&P 500 dropped 0.21%, Dow Jones moved 0.43% lower while Nasdaq gained 0.25% and Russell 2000 moved 0.40% higher

- US 10-year yields briefly breached 4% yesterday but have pulled back to 3.97% since

- US dollar gained after White House official Brian Deese said he does not expect major economies to agree on an accord aimed at weakening USD as it was the case in 1985

- Indices from Asia-Pacific slumped during the session today. Nikkei dropped 2%, S&P/ASX 200 moved 0.7% lower while Kospi traded 2.7% down. Indices from China traded 0.2-2.5% lower

- DAX futures point to a lower opening of the European cash session today

- US Treasury Secretary Yellen said that financial markets are operating normally and that she does not see any liquidity issues in the markets

- Moody’s said that new UK fiscal measures are credit negative as tax cuts are massive but lack funding

- According to BoJ minutes, BoJ members see fears of global slowdown intensifying and price increases in Japan broadening. Members see need to carefully watch impact on rapid FX moves on inflation

- Goldman Sachs expects Brent price to average $100 in Q4 2022, down from previous forecast of $125. Bank also expects average Brent price in 2023 at $108, also down from $125 previously expected

- Australian retail sales increased 0.6% MoM in August (exp. 0.5% MoM)

- API report pointed to a 4.15 million barrel build in US oil inventories (exp. +0.3 mb)

- Cryptocurrencies are pulling back. Bitcoin trades 1.1% lower, Ethereum drops 2.8% while Ripple trades 4% lower

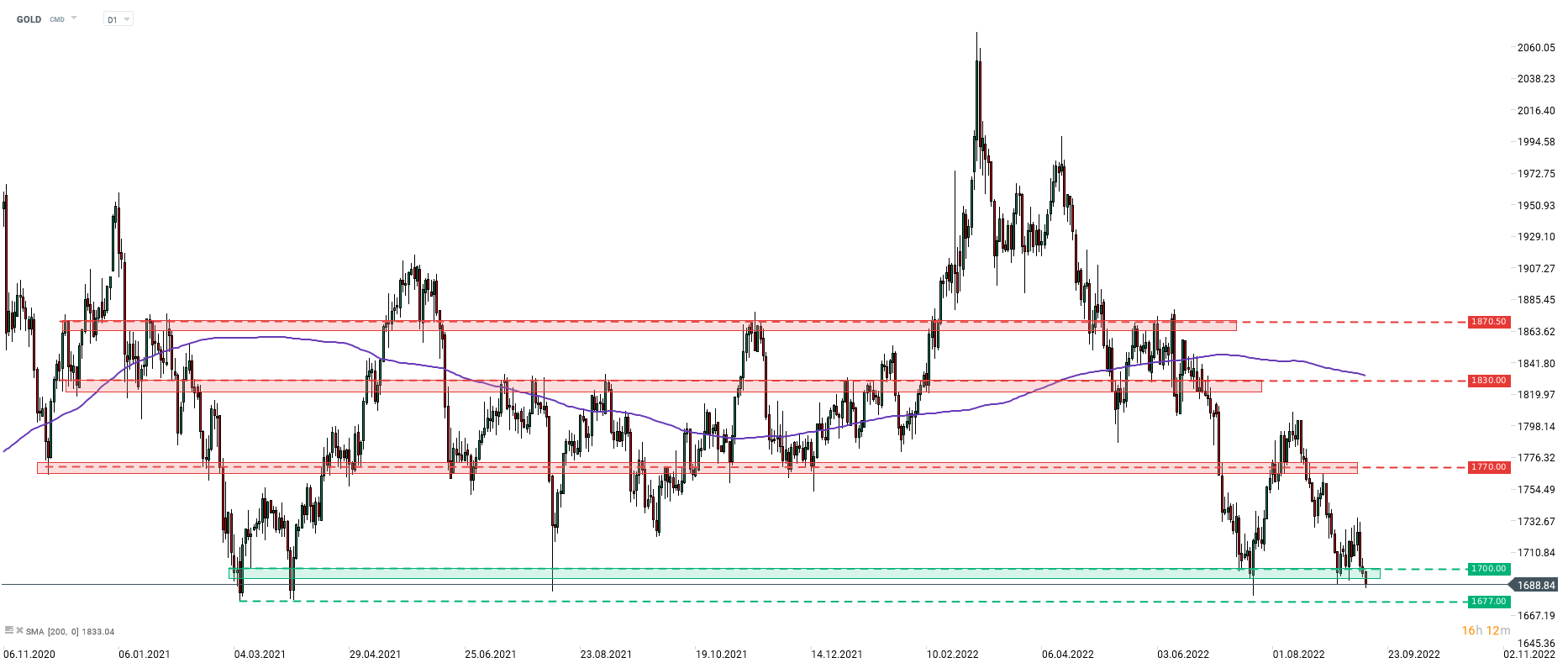

- Commodities trade lower amid USD strengthening. Brent and WTI trade around 0.7% lower. Gold drops 0.3% while silver trades 1.2% down

- USD and JPY are the best performing major currencies while NZD and AUD lag the most

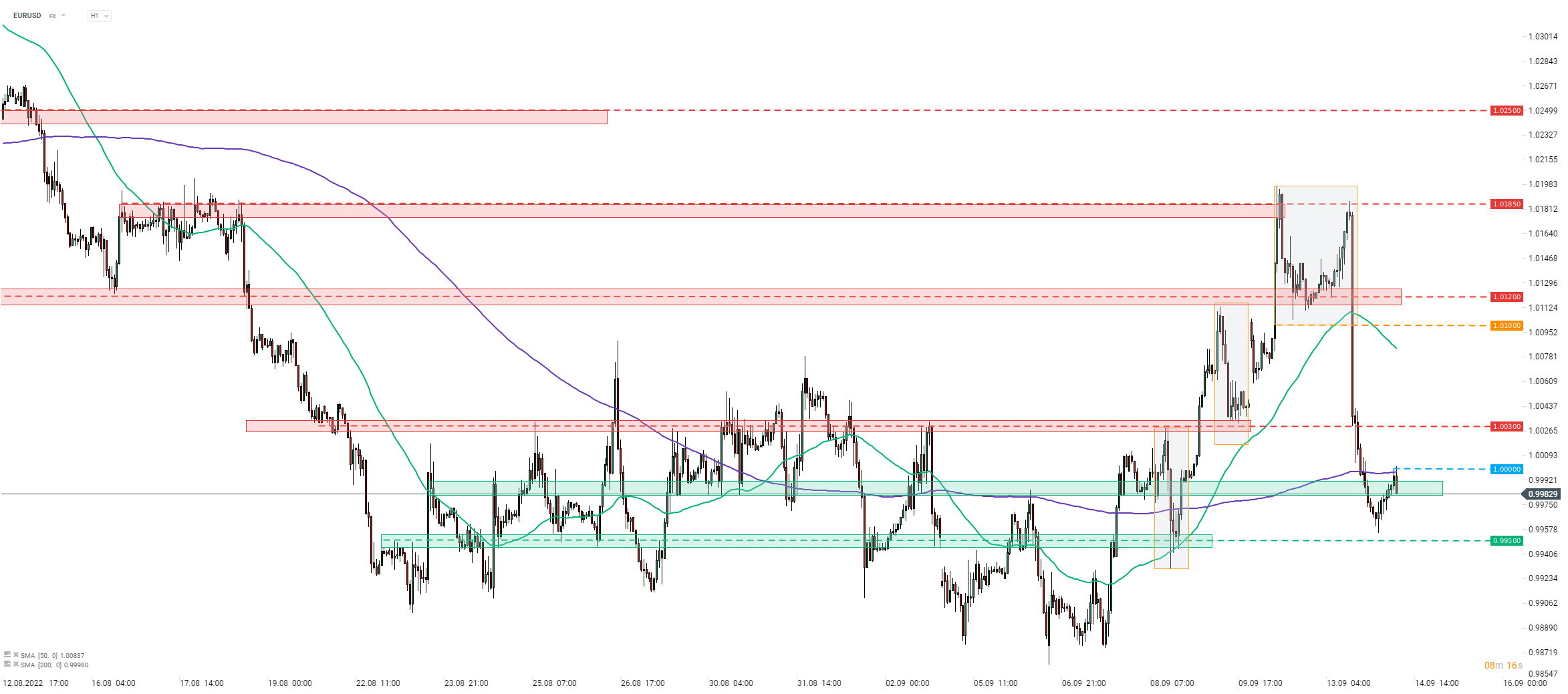

EURUSD painted a fresh 20-year low near 0.9550 as the USD rally resumed

EURUSD painted a fresh 20-year low near 0.9550 as the USD rally resumed

Rally on USDJPY eased somewhat as of late and the pair started to trade sideways in the 142.70-143.65 range. This is interesting as US yields (inverted TNOTE overlay on the chart) continue to move higher. Such development can be reasoned with uncertainty ahead of the Fed decision on Wednesday and BoJ decision on Thursday.

Rally on USDJPY eased somewhat as of late and the pair started to trade sideways in the 142.70-143.65 range. This is interesting as US yields (inverted TNOTE overlay on the chart) continue to move higher. Such development can be reasoned with uncertainty ahead of the Fed decision on Wednesday and BoJ decision on Thursday.

Ethereum dropped to a 2-month low over the weekend and is testing $1,275-1,300 support zone now. Moods on the overall cryptocurrency market are poor as well with Bitcoin down over 3% and Ripple trading 7% lower.

Ethereum dropped to a 2-month low over the weekend and is testing $1,275-1,300 support zone now. Moods on the overall cryptocurrency market are poor as well with Bitcoin down over 3% and Ripple trading 7% lower.

S&P 500 (US500) has fully erased the recent jump and is now testing the 3,900 pts support zone. Selling intensified yesterday after the close of the Wall Street session as an earnings report from FedEx pointed to weakness in Asian and European business.

S&P 500 (US500) has fully erased the recent jump and is now testing the 3,900 pts support zone. Selling intensified yesterday after the close of the Wall Street session as an earnings report from FedEx pointed to weakness in Asian and European business.

Oil is trading lower at the beginning of a new week. News on Russian price caps, Russian retaliation for it or lack of progress in Iran talks fail to lift crude prices signaling that worries over global growth are playing a key role now.

Oil is trading lower at the beginning of a new week. News on Russian price caps, Russian retaliation for it or lack of progress in Iran talks fail to lift crude prices signaling that worries over global growth are playing a key role now.