Daily Analysis 15 november 2022

- US indices finished yesterday’s trading lower after a volatile session. S&P 500 dropped 0.89%, Dow Jones moved 0.63% lower and Nasdaq declined 1.12%. Russell 2000 traded 1.14% lower

- Indices from Asia-Pacific traded mixed today. Nikkei, Kospi and indices from China gained while S&P/ASX 200 and NIfty 50 dropped

- DAX futures point to a slightly lower opening of the European cash session today

- Fed’s Barr said that while tightening had an adverse impact on US economic outlook, inflation still remains too high

- ECB’s Villeroy said that ECB will continue to raise rate but pace of the process may slow

- RBA said in minutes that both – quicker pace of rate hikes and pause to tightening cycle – remain an option

- According to UK Times, UK Prime Minister Sunak is preparing to increase living wage from 9.50 GBP per hour to 10.40 GBP per hour

- Chinese retail sales dropped 0.5% YoY in October (exp. +1.0% YoY). Industrial production was 5.0% YoY higher (exp. 5.1% YoY) while urban investments increased 5.8% YoY (exp. 5.9% YoY). China’s statistic office said that economic recovery slowed on the back of Covid outbreaks

- Japanese economy contracted at an annualized pace of 1.2% in Q3 2022 (exp. +1.1%)

- Japanese industrial production dropped 1.7% MoM in September (exp. -1.6% MoM)

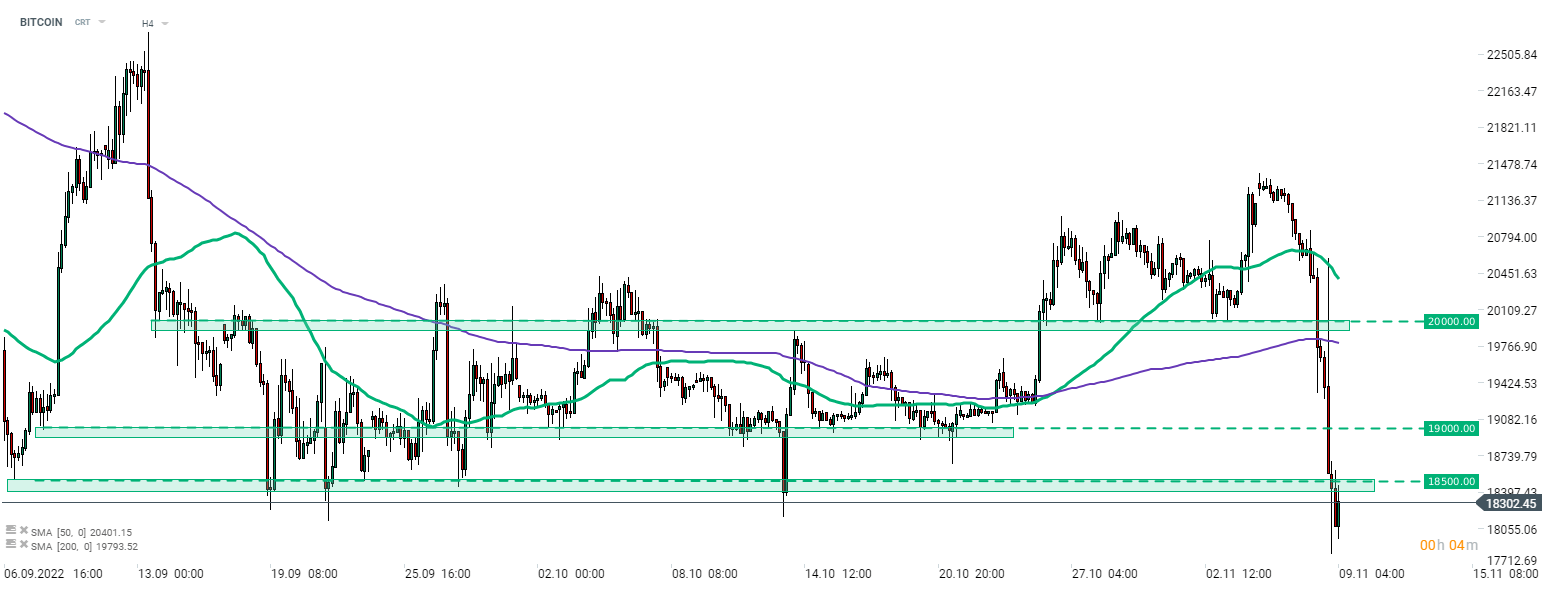

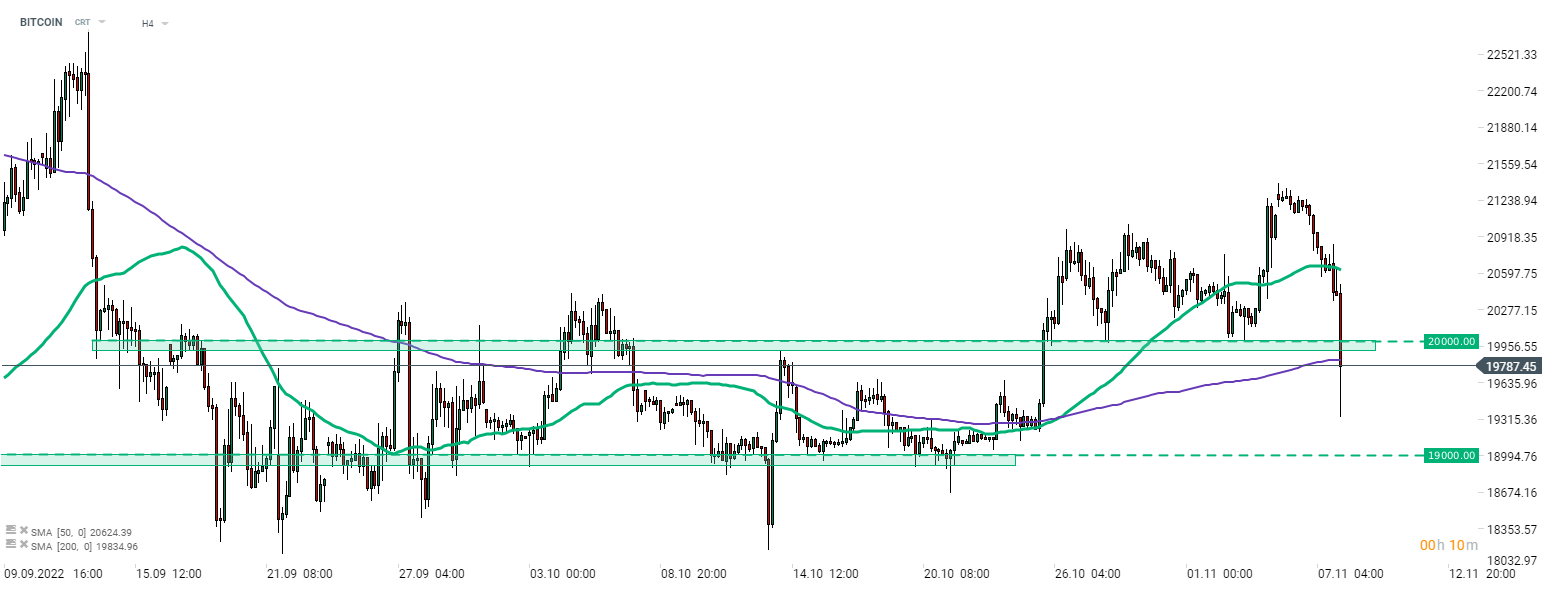

- Cryptocurrencies are holding more or less stable, with the majority of coins posting small gains. Bitcoin trades 2% higher while Ethereum gains 2.8%

- Oil is trading little changed while natural gas price rises

- Precious metals trade slightly higher – platinum gains 0.1%, silver adds 0.2% and gold trades flat

- NZD and GBP are the best performing major currencies while JPY and CHF lag the most

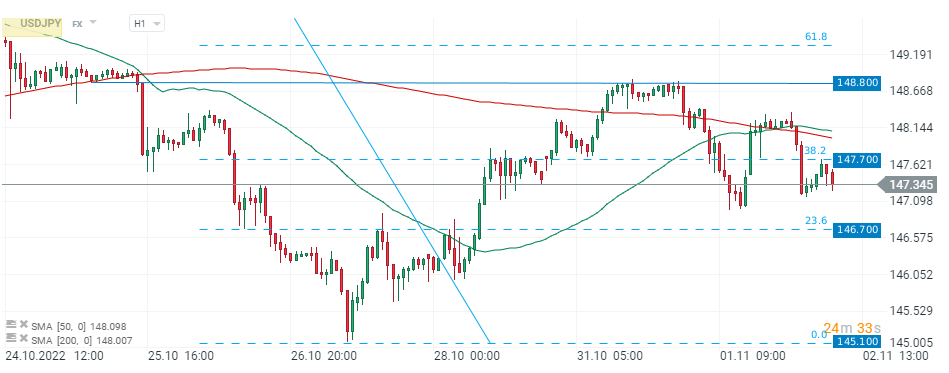

USDJPY extends recovery today, supported by weaker-than-expected GDP reading from Japan. The pair continues to recover after a failed attempt of breaking below the 61.8% retracement.

USDJPY extends recovery today, supported by weaker-than-expected GDP reading from Japan. The pair continues to recover after a failed attempt of breaking below the 61.8% retracement.

35796346713+

35796346713+ support@Forextk.com

support@Forextk.com